Year-end is a crucial time for bookkeepers and accountants. It is also a hectic time as it involves multiple reviews of their books, reconciling transactions, and cross-checking statements. These year-end bookkeeping tasks are essential for producing accurate financials, preparing for tax obligations, ensuring compliance, and giving business owners the clarity they need to make informed decisions for the year ahead. Finance teams, already stretched thin by last-minute client demands, might find themselves at the brink of burnout during this time. This is why it is important to plan ahead, make a checklist, and seek help from an external party if needed. A clear end of the year accounting checklist helps firms stay compliant, avoid last-minute stress, and close their books accurately. In this article, we share a practical financial year-end checklist to help you stay organised, reduce errors, and close the year with confidence.

What is Year-End Closing?

Year-end closing is a structured process that includes a comprehensive financial year-end closing checklist to ensure all records are reviewed and finalised before the new accounting period begins. It involves reviewing, reconciling, and confirming all financial transactions to ensure your books accurately reflect the business’s performance for the year. This includes tasks such as matching bank statements, verifying accounts receivable and payable, updating fixed asset records, adjusting accruals, and preparing final financial statements. A well-prepared year-end accounts checklist also helps firms identify discrepancies early and prevent reporting errors before final submissions.

Financial Year-End Closing Checklist

As mentioned before, there are multiple tasks to be carried out and less time during the crucial year-end period. Teams face many challenges that hinder the successful closing of books, leading to non-compliance, delayed tax filings, client dissatisfaction, possible penalties, and blind decision-making for the next year. Some of the common difficulties encountered during the closing period are as follows.

Human error

There is absolutely no room for error in bookkeeping, especially during end-of-year bookkeeping checklist activities. Even the slightest mistake can cost a hefty penalty. However, human error cannot be avoided, especially in the year-end rush, even by the most organised and experienced bookkeeper.

Incomplete records

A common challenge in closing the year-end accounts is incomplete records, missing bills, and receipts, and accountants and bookkeepers often have to chase vendors, suppliers and clients for all the updated documents.

Manual data entry

Manual data entry leaves room for small but costly mistakes that can throw off your books. By adopting automation or partnering with a reliable, tech-enabled outsourcing provider, businesses can significantly reduce errors and maintain cleaner, more accurate financial records.

Communication gaps with clients

Oftentimes, there is a communication gap between bookkeepers and clients, leading to missed documents, incomplete information, and unrecorded transactions. This slows down the reconciliation process and increases the risk of year-end inaccuracies.

Time pressure & staff shortage

Bookkeeping firms often face a shortage of personnel during the year-end close. Add to this the high volume of last-minute transactions and the time crunch, and you have a recipe for disaster. This resource strain not only slows down turnaround time but also increases the likelihood of oversight and errors.

Year-End Closing Checklist

The simplest way to ensure a seamless year-end close is to plan ahead and follow a year-end accounting checklist. To make things easier, we have prepared a practical year-end checklist for bookkeepers, which will help ensure timely submissions of books and a smooth transition into the new year.

Year-End Accounts Checklist

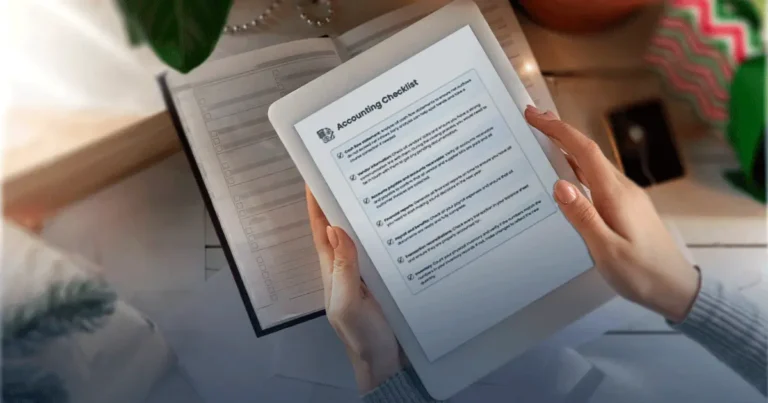

- Cash flow statement: Analyse all cash flow statements to ensure net outflows do not exceed net inflows. Early analysis can help spot trends and take a course correction if needed.

- Vendor information: Check all vendors’ data and ensure you have a strong communication line with them. During the closing process, you would need to be in touch with them to get any pending documentation.

- Accounts payable and accounts receivable: Verify all accounts receivable and payable to confirm that all vendor and supplier bills are paid and all customer invoices are collected.

- Financial reports: Generate all financial reports on time to ensure you have all you need to start making sound decisions in the next year.

- Payroll and benefits: Check all your payroll expenses and ensure that all documents are ready and fully complete.

- Transaction reconciliations: Check every transaction in your balance sheet and ensure they are properly accounted for.

- Inventory: Count your physical inventory and verify if the numbers match the numbers in your inventory records. If not, make changes to reflect the new quantity.

Tax Checklist

Tax preparation forms a critical part of any end of the year accounting checklist, particularly for firms managing multiple clients with varying compliance deadlines. Proper planning ensures accurate submissions, minimises last-minute corrections, and reduces the risk of penalties.

- Make a list of the tax forms you need to file: Ensure your team has a complete inventory of all tax forms required for accurate and timely lodgement.

- Collect or arrange all relevant documents you need: Request, organise, and securely store every document needed to prepare year-end tax filings.

- Identify any tax deductions or credits: Review records to spot eligible deductions or credits that can minimise tax liability.

- Request extensions for filing if required: Assess if you need more time and proactively submit extension requests to avoid penalties.

These year-end processes can become even more structured in sectors like education, where accurate reporting and compliance depend on well-organised education accounting systems.

Document Checklist

- Bank statements: Gather all business bank statements for the full financial year to support reconciliations.

- Credit card statements: Collect all business credit card statements to verify expenses and match transactions.

- Inventory records: Conduct and document an accurate year-end stocktake, ensuring records align with accounting data.

- Previous year’s financial statements & tax return: Keep last year’s accounts and CT600 return handy for reference and comparative analysis.

- Loan statements & finance agreements: Download year-end loan summaries showing outstanding balances and interest paid.

- Merchant service statements (e.g., Stripe, PayPal, Square): Compile reports of all sales processed through payment platforms.

- VAT records: Ensure all VAT returns, VAT summaries, and supporting documents for the year are available.

- Payroll year-end reports: Gather all PAYE records, FPS/EPS submissions, P60s, and other payroll summaries.

- Supplier and contractor statements: Collect statements from vendors and subcontractors to reconcile outstanding amounts.

- Customer statements: Ensure customer balances match the statements or sales ledger.

- Fixed asset register & purchase invoices: Update your fixed asset register and collect any documents for asset additions or disposals.

- Expense receipts & employee reimbursement claims: Organise all business-related receipts and staff expense submissions.

- Insurance documents: Maintain copies of business insurance policies for verification of prepaid amounts.

- Lease agreements (property, vehicles, equipment): Ensure all lease statements and agreements are available for adjustments and disclosures.

- Direct debit and standing order summaries: Download lists of all recurring payments for cross-checking liabilities and expenses.

- HMRC correspondence: Keep all notices, reminders, or communications received during the year.

In Conclusion

Year-end closing doesn’t have to be overwhelming. With the right systems, a clear bookkeeping year-end checklist, and reliable support, bookkeepers and accountants can navigate the busiest season with accuracy and confidence. Following a structured end of financial year checklist for bookkeepers ensures stronger compliance, better reporting accuracy, and smoother transitions into the new financial year. By proactively organising records, closing gaps in communication, and strengthening processes, firms set themselves and their clients up for a stronger financial year ahead. If your firm needs additional capacity or expert assistance during peak periods, befree’s specialised bookkeeping outsourcing services can help you streamline operations, reduce stress, and deliver flawlessly every time.